A blockchain is often mistakenly thought to be a large book of financial transactions, but that is not the case. Blockchain technology is actually a set of protocols that govern digital transactions like bitcoin and ethereum. This blockchain can't be altered from the outside - which means it's an incorruptible digital ledger of all transactions in the network. As such, it has a lot of promise for various industries

What Is A Blockchain?

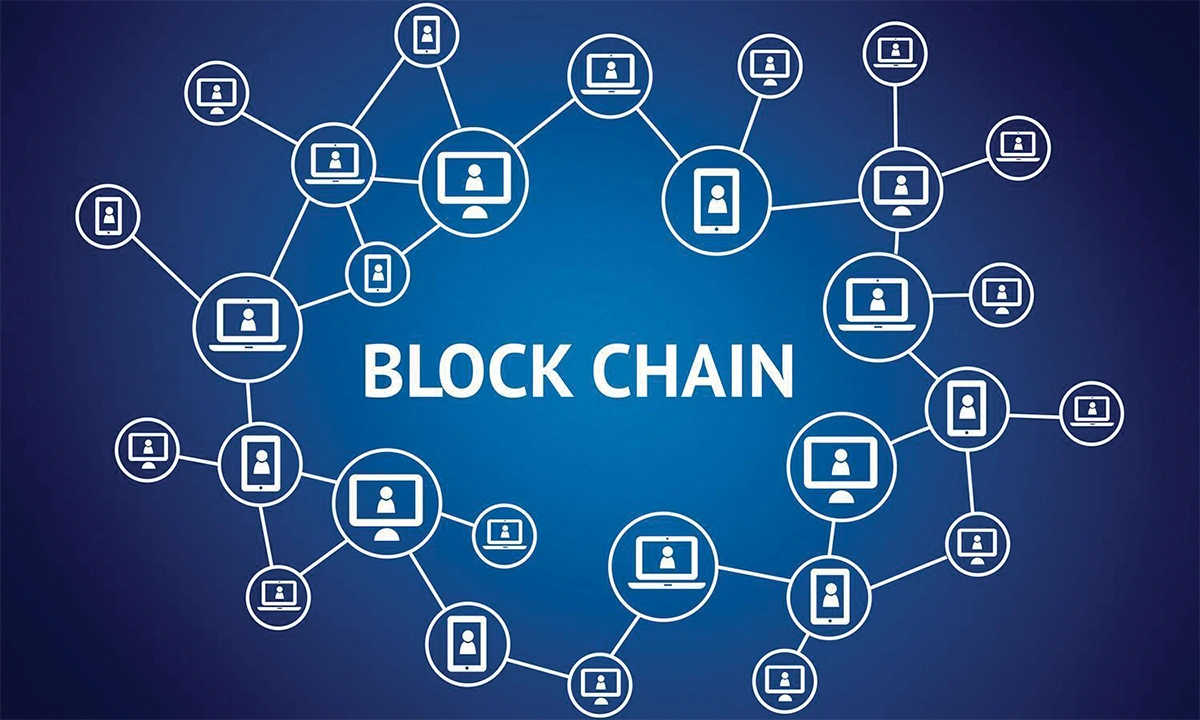

A blockchain is a distributed database that allows for secure, transparent and tamper-proof transactions. A blockchain network consists of a peer-to-peer network of computers that are connected to each other. Transactions are verified and recorded in a chronological order using cryptography.

Once a transaction is verified, it is added to the blockchain ledger. This ledger is constantly growing as “completed” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin, Ethereum and other cryptocurrencies use blockchains to control their own operations and create an open, transparent and decentralized network.

How Does The Blockchain Work?

Simply put, a blockchain is a digital ledger of all cryptocurrency transactions. It is constantly growing as “completed” blocks are added to it with a new set of recordings. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. Bitcoin and most other cryptocurrencies use blockchain technology to facilitate peer-to-peer transactions without the need for third parties like banks.

How does the blockchain work?

To create a new block, miners must solve complex mathematical problems. When they solve one, they are rewarded with cryptocurrency (Bitcoin currently rewards miners with 12.5 bitcoins). To keep track of who solved which problem, each miner keeps a copy of the briansclub (which includes the hash of the previous block) along with their own copy of the block contents. Whenever someone wants to send bitcoin to someone else, they must include their copy of the block header with their transaction. The network then verifies that this copy matches what’s in everyone else’s heads – if not, it gets rejected. As more and more people join the network, it becomes harder and harder for someone to falsely claim a block header as their own.

Is blockchain perfect?

No – there are some potential weaknesses with blockchain that researchers are still exploring. For example, because every node on the network keeps track of every transaction, it’s possible that somebody could generate millions or even billions of fake

The Different Types Of Blockchains

There are many different types of blockchains, and each has its own unique features. This guide will explain the different types of blockchains and their benefits.

Bitcoin is the most well-known blockchain technology. Bitcoin operates on a distributed ledger, which is a database that is constantly growing as new blocks are added to it. Transactions on a bitcoin blockchain are verified by network nodes through cryptography and recorded in a public registry. Bitcoin was created in 2009 by an anonymous person or group of people who called themselves Satoshi Nakamoto.

Ethereum is another popular blockchain technology. briansclub.cm operates on a blockchain platform with smart contracts that allow for decentralized applications to be built and run without any third party involvement. Smart contracts are self-executing contracts that can automatically execute specified actions when certain conditions are met. Ethereum was created in 2015 by Vitalik Buterin, who also invented bitcoin mining software.

What Are Some Applications For Blockchain Technology?

There are many potential applications for blockchain technology, including but not limited to:

-Distributed ledgers that can be used to track the ownership of assets and document transactions between parties;

-A secure way to verify the legitimacy of digital signatures;

-A decentralized platform for issuing and selling cryptocurrencies;

-An encrypted database that allows users to share information securely without having to trust third parties.

Conclusion and Benefits of Blockchain Technology

Blockchain technology is revolutionizing the way transactions are conducted between two or more people. It is a distributed ledger that stores transactions and allows participants to interact without the need for a third party. Transactions are verified by network nodes and then added to the blockchain. This creates an unalterable record of all transactions that have ever taken place.

The benefits of using blockchain technology include:

- Reduced costs: Because blockchain is a decentralized system, there is no need for third-party verification or settlement. This reduces transaction costs and makes it easier for parties to conduct business with each other.

- Increased security: Because blockchain is tamper-proof, it ensures that data remains confidential. This protects businesses from cyberattacks and ensures that customers’ data remains safe.

- Greater transparency: Blockchain technology can help increase transparency by making it easier to track the origin of goods and identify fraudsters. It can also help businesses to comply with anti-money laundering regulations.

No comments yet