In the intricate landscape of taxation, understanding the applicability of the Goods and Services Tax (GST) is crucial for individuals, businesses, and organizations alike. This comprehensive guide aims to shed light on the nuances of GST registration, classification, and the diverse scenarios where GST becomes applicable.

Obtaining GST Registration: Commencing a business journey requires obtaining GST registration, wherein a unique 15-digit Goods and Services Tax Identification Number (GSTIN) is assigned by the Central Government post-registration.

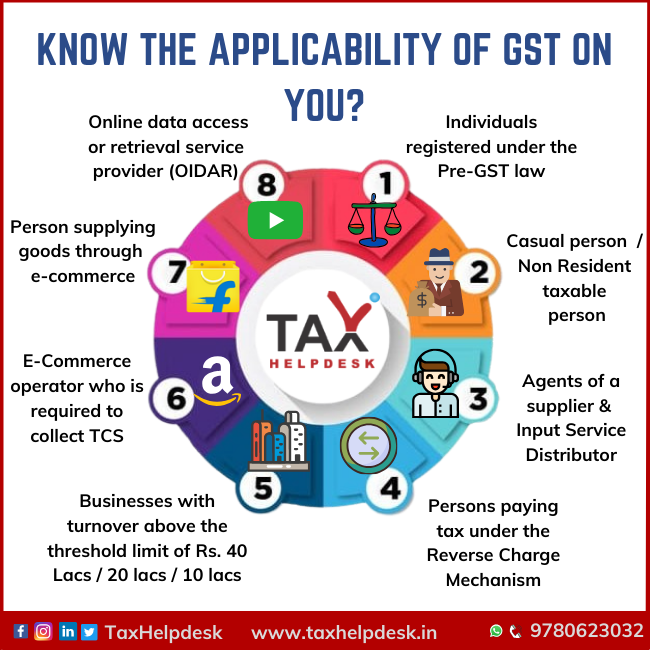

Who Needs GST Registration? As per the GST Act, several entities are mandated to obtain GST registration. These include suppliers exclusively engaged in goods, those with prior registrations under the erstwhile law, and those involved in business transfers.

Compulsory GST Applicability: Beyond the threshold limits, certain entities are obligated to register for GST, such as casual taxable persons, non-resident taxable persons, inter-state suppliers, service providers, and those liable under the reverse charge mechanism. This also encompasses TDS/TCS deductors, agents and suppliers of Input Service Distributors, and online data access or retrieval service providers.

Casual Taxable Persons: Defined as individuals or businesses occasionally involved in transactions without a fixed place of business, casual taxable persons undergo temporary registration, valid for the specified period of 90 days, with the possibility of extension.

Non-Resident Taxable Persons: Individuals or businesses lacking a fixed place of business in India, engaging in occasional transactions, also require temporary GST registration, valid for the specified period of 90 days, extendable for an additional 90 days.

Inter-State Suppliers and Service Providers: Inter-state suppliers of goods and services, irrespective of turnover, must register for GST. Additionally, GST applies to all services provided by businesses and professionals.

Reverse Charge Mechanism (RCM): Entities liable under RCM, where the recipient pays the tax liability, are obligated to register for GST.

Agents and Suppliers of Input Service Distributors: Entities involved in distributing credit for input services must apply for GST registration.

TDS/TCS Deductors and Online Service Providers: Entities deducting TDS or collecting TCS, and online data access or retrieval service providers, fall within the ambit of GST applicability.

Understanding these facets of GST applicability is crucial for navigating the complex tax landscape. Stay informed and compliant by consulting experts and utilizing tools to streamline the registration process.

Explore our GST consultation services and ensure your business stays GST-compliant. Register your GST today and simplify your tax journey!

No comments yet