Table of Contents

- Introduction

- The Importance of Financial Education

- Defining Assets and Liabilities

- Examples of Assets

Real Estate

Stock Investments

Business Ownership - Examples of Liabilities

Mortgage Debt

Consumer Debt

Car Loans - The Cash Flow Quadrant

- Conclusion

- FAQs

Introduction

"Rich Dad Poor Dad" by Robert Kiyosaki is a renowned financial education book that has impacted the lives of millions. One of its fundamental concepts revolves around understanding assets and liabilities. In this comprehensive review, we will delve into the examples of assets and liabilities presented in the book. We'll explore why financial education matters, define assets and liabilities, provide detailed examples, and discuss how this knowledge fits into the larger framework of financial independence.

The Importance of Financial Education

Before we dive into assets and liabilities, it's crucial to emphasize the significance of financial education. In the traditional education system, many individuals are not taught essential financial principles, leaving them ill-prepared to navigate the complexities of money management.

Understanding how money works is the first step towards achieving financial freedom. "Rich Dad Poor Dad" argues that financial education is often more valuable than formal education when it comes to building wealth. This book encourages readers to seek out financial knowledge actively.

Defining Assets and Liabilities

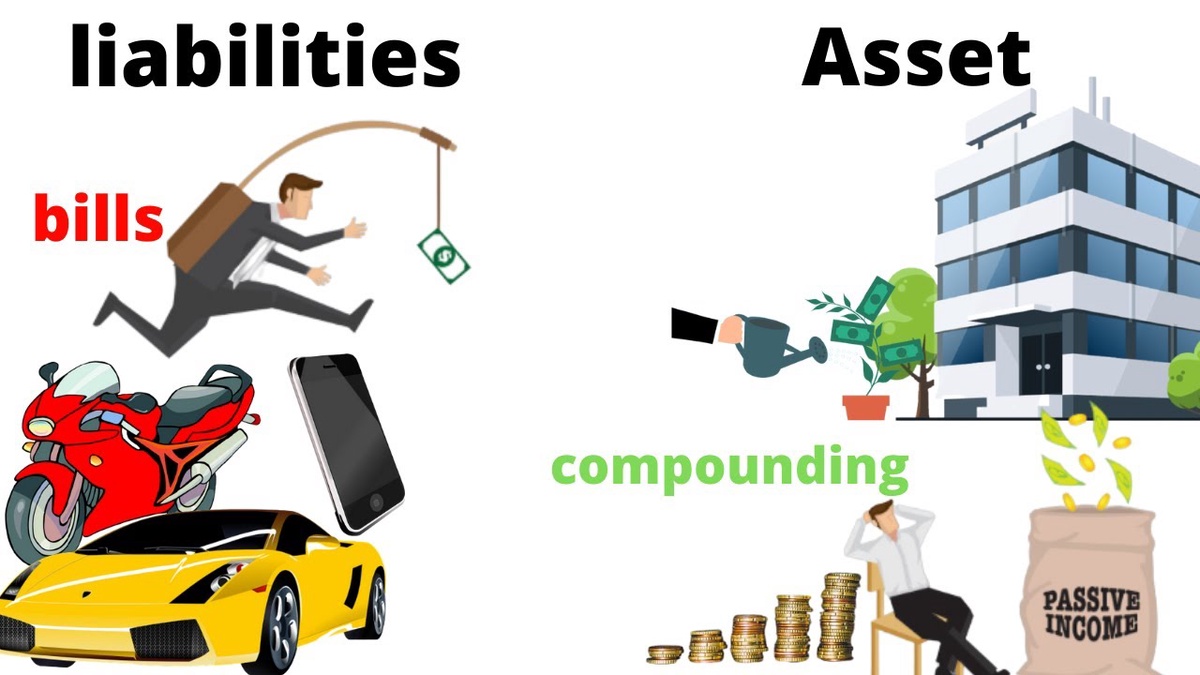

To comprehend the examples presented in the book, we need a clear understanding of what assets and liabilities are:

-

Assets: Assets are items of value that put money in your pocket. They generate income or appreciate over time.

-

Liabilities: Liabilities are items of cost that take money out of your pocket. They typically involve ongoing expenses.

Examples of Assets

Real Estate

Real estate is a classic example of an asset. Owning property can provide several financial benefits, including rental income, property appreciation, and potential tax advantages. Whether it's residential or commercial real estate, it has the potential to generate a steady stream of income.

Hyperlink: Real Estate Investment Benefits

Stock Investments

Investing in stocks can also be a powerful asset-building strategy. When you purchase shares of a company, you become a partial owner, and if the company performs well, your shares may increase in value. Additionally, some stocks pay dividends, providing a source of passive income.

Hyperlink: Stock Market Basics

Business Ownership

Starting or owning a successful business can be a substantial asset. A well-run business can generate significant profits and build long-term wealth. Entrepreneurs have the potential to create assets that provide financial security and freedom.

Hyperlink: Starting a Small Business

Examples of Liabilities

Mortgage Debt

While owning real estate can be an asset, the mortgage on that property is a liability. Mortgage debt involves regular payments and interest expenses that take money out of your pocket. It's essential to manage mortgage debt wisely to maximize the benefits of property ownership.

Hyperlink: Mortgage Basics

Consumer Debt

Consumer debt includes credit card balances and personal loans. These liabilities often come with high-interest rates, leading to substantial monthly payments. They can become a financial burden, especially if not managed carefully.

Hyperlink: Credit Card Debt Management

Car Loans

Car loans are another common liability. While a vehicle is a necessity for many, financing it through a loan involves ongoing payments and interest costs. Understanding the impact of car loans on your finances is crucial for making informed decisions.

Hyperlink: Car Loan Basics

The Cash Flow Quadrant

Robert Kiyosaki introduces the Cash Flow Quadrant as a framework for understanding how individuals earn income. It categorizes people into four groups: Employees, Self-Employed, Business Owners, and Investors. This concept ties directly into the discussion of assets and liabilities, as each quadrant has a different approach to managing their financial affairs.

Conclusion: Achieving Financial Freedom Through Asset Accumulation

In conclusion, "Rich Dad Poor Dad" offers valuable insights into the world of assets and liabilities. Understanding the difference between the two is fundamental to building wealth and achieving financial independence. By actively seeking financial education, individuals can make informed decisions about their finances, ultimately leading to a more secure and prosperous future.

FAQs

Q1: What are some other examples of assets mentioned in the book?

- The book also discusses assets like intellectual property (e.g., patents and royalties) and investments in businesses.

Q2: Can you provide more information on the Cash Flow Quadrant?

- The Cash Flow Quadrant categorizes income earners into four groups: Employees, Self-Employed, Business Owners, and Investors. Each group has a different approach to earning and managing money. You can learn more about it here.

Q3: How can I start building assets and reducing liabilities?

- To begin building assets, consider investing in assets like stocks, real estate, or starting a business. Simultaneously, work on reducing liabilities by managing debt wisely and avoiding unnecessary expenses.

No comments yet