When it comes to life insurance, your price depends on several factors.

Did you know that insurance companies place people with the same age, gender, and coverage amount in different categories?

When you apply for life insurance, your insurer will put you in certain categories based on your relative risk. They assess the risk factor by evaluating your health and lifestyle. This is known as the “rating category.”

The healthiest people get the lowest insurance rates. This is because of their low-risk profile.

To determine this, insurers will evaluate your medical problems, dietary habits, or lifestyle that can put you at risk of dying early. Based on this evaluation, they determine your rating class. If you are perfectly healthy, do not have a significant or longstanding illnesses such as diabetes, your weight and cholesterol are in perfect range, and you do not smoke or consume tobacco or alcohol, you will be put in the lowest risk category.

What are the various rating classes or categories?

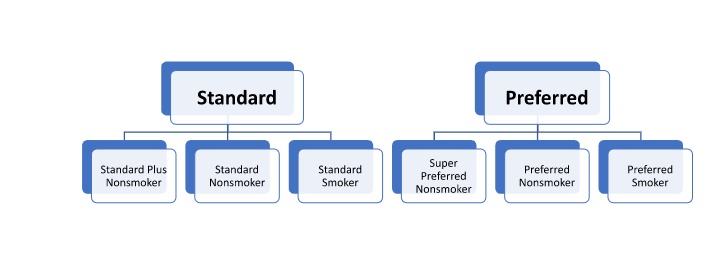

Insurance companies have different rating classes. The names of these categories may differ from company to company, but essentially, they are broadly classified into two groups: Standard vs Preferred life insurance categories.

-

Standard Category

Any person with an average life expectancy and relatively low-risk factors is included in this category.

-

Preferred Category

Only the people with the healthiest lifestyle and lowest risk are put into this category. This category helps them qualify for the lowest rates.

Now, these broad categories are further sub-divided into several generic sub-categories:

Now, let’s discuss each of these categories in more detail:

Standard Category

-

Standard Plus Non-smoker:

- This category has people who are non-smokers

- They are generally in good health but not excellent to be put in the Preferred category

- Hypertensive patients who are receiving treatment and whose blood pressure readings are in normal ranges are also included in this category

-

Standard Non-smoker:

- This category is for normal people with an average life expectancy

- If you are overweight or if you are seeking treatment for hypertension and type 2 diabetes, you will be accepted in this category

- People who have someone in their family who passed away before the age of 60 due to heart disease or cancer are also included in this category

-

Standard Smoker:

This category is for smokers with an average life expectancy and who have a risky family medical history too. They may be overweight, hypertensive, and diabetic too.

Preferred Category

-

Super Preferred Non-smoker/ Elite Preferred Non-smoker:

People who are super healthy and who lead an extremely healthy lifestyle are included in this category. To be a part of it:

- You should not have smoked nicotine or other nicotine substitutes for over 5 years

- You should have a normal BMI according to your height and gender

- You should have a normal blood pressure

- Your cholesterol and sugar readings should be normal

- You should have a clean medical history

- You should not have a blood relative dying of heart disease or cancer before the age of 60

- Your driving record should be clean, and you should not have a history of the suspension of your driving license

- You should not have a DUI conviction in the last 5 years

- You should not have any record of accidents or more than two moving violations in the last 3 years

-

Preferred Non-smoker:

This category is for people with a healthy and great lifestyle, but it gives slight lenience on several factors.

- You should not be a habitual smoker, but some companies allow occasional cigar usage and still keep you in this category if other things are all right too. But your nicotine tests should be negative.

- Your occasional ups and downs with blood pressure, cholesterol, and weight readings can be overlooked as long as things are okay according to your BMI.

- You should not have a blood relative dying of heart disease or cancer before the age of 60

- Generally, you do not need to be a fitness freak or a super-model to be in this category. But some general factors need to be in control so that you can be accepted in this class. And you can qualify for the second-best insurance rates.

-

Preferred Smoker:

This category includes smokers with other health dynamics in control and with a clean medical, family, and driving history too.

People who quit smoking and have not smoked nicotine for over 5 years can also qualify for the best insurance rates for smokers. If you quit smoking 3 years ago, you will be eligible to qualify for the second-best smoking rates. But if you quit smoking 1 year ago, you will be disqualified from the Preferred category and will be eligible for Standard non-smoker rates.

What happens if you are not eligible for any of the categories?

People with type 1 diabetes, uncontrolled type 2 diabetes, uncontrolled hypertension, or with a significant heart ailment like cancer, or other life-threatening illness may not be accepted in the Standard category. But they are still eligible for insurance. So, insurance companies place these people according to another rating system that’s called a “table rating.”

Some insurers use numerals while others use alphabets to classify the table rating system.

I someone is given the 1st table rating, or an A according to a different company, their insurance rate will be slightly lower than the person who is in the 2nd or B category.

The standard rate is often increased by 25% for every table rating as it goes higher. Therefore, a C on the table denotes a rate plus 75% over the benchmark.

A temporary extra fee, known as a "flat extra" may occasionally be tacked on by an insurance company. For instance, say a cancer survivor gets $500,000 of life insurancecoverage . They will be charged an additional $5 for every $1000 of the total coverage for 5 years. This means that they will have to pay an additional amount of $2500 every year for the first 5 years along with their usual insurance rate.

Conclusion

If the insurance provider determines that you do not meet the requirements at a discounted rate, you can ask why. In some circumstances, the insurer might not have the complete information it required. If you give it to them, they'll sometimes re-evaluate your premium. Regardless, it’s best to get insurance coverage sooner than later, while you are still in good health and your price is affordable. A licensed life insurance broker can help you find the best coverage at the best price.

No comments yet