In the complex landscape of income tax regulations, Section 194D plays a crucial role in governing the deduction of Tax Deducted at Source (TDS) on insurance commission. Let’s delve into the intricacies of this section, exploring its key provisions, instances of deduction, rates, and consequences of non-compliance.

Understanding Section 194D

Section 194D mandates TDS on payments made to a resident for generating insurance business. This includes commissions, remuneration, or rewards associated with activities such as soliciting, obtaining insurance business, and the continuance, renewal, or revival of insurance policies.

Cases Requiring TDS under Section 194D

TDS is applicable when payments in the form of remuneration or rewards are made to residents for insurance-related activities. This encompasses commission payments linked to soliciting or obtaining insurance business and the continuance, renewal, or revival of insurance policies.

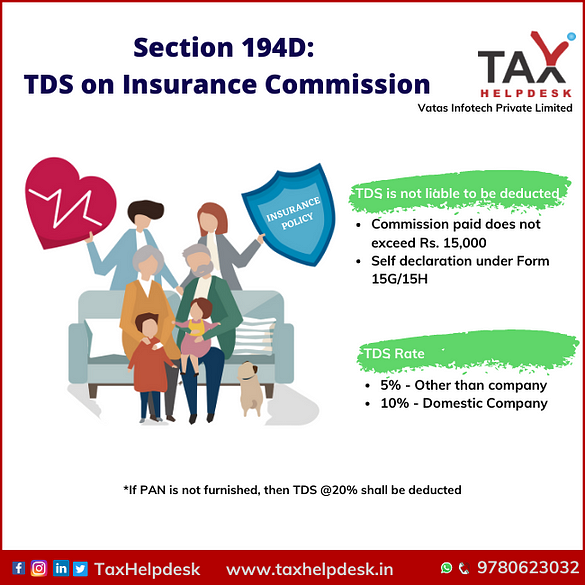

Instances Exempt from TDS under Section 194D

Two specific scenarios exempt payments from TDS under Section 194D:

- The commission paid does not exceed Rs. 15,000.

- Self-declaration under Form 15G/15H.

TDS Deduction Events under Section 194D

TDS on insurance commission is deducted at the earlier of two events:

- At the time of crediting the commission to the payee’s account.

- At the time of making payment in cash, cheque, or kind.

TDS Rates under Section 194D

The rates of TDS under Section 194D vary based on whether the PAN is furnished or not. For persons other than companies, it is 5% with PAN and 20% without, while domestic companies face rates of 10% with PAN and 20% without. Surcharge or Secondary and Higher Education Cess is not applicable to these rates.

Non-Deduction or Lower Rate Application

Individuals receiving commission can apply in Form 13 to the Assessing Officer for a certificate authorizing non-deduction or a lower rate of tax deduction. Section 206AA(4) mandates PAN submission for such applications.

Time Limits and Due Dates

TDS on insurance commission must be deposited by the 7th of the following month. TDS certificates, summarizing payments and TDS details, must be issued quarterly, with specific deadlines. Additionally, quarterly TDS returns must be filed by the specified dates.

Consequences of Non-Compliance

Failure to comply with TDS regulations attracts interest at 1.5% on the outstanding amount. Non-compliant individuals are also ineligible to claim deductions for expenses from their business income.

In conclusion, understanding and adhering to Section 194D is essential for those involved in insurance-related transactions. From TDS rates to due dates, this comprehensive guide provides insights into the intricacies of TDS on insurance commissions, ensuring compliance with the Income Tax Act. For further clarification or expert consultation on TDS matters, readers are encouraged to engage with TaxHelpdesk through various communication channels.

No comments yet